Health IQ is an insurance broker that markets to people who make healthy choices by offering them cheaper term life insurance.

In this article, I’ll explain how Health IQ works and whether it’s a good idea for you to give it a shot.

Table of Contents

- Health IQ Review: Quick Look

- What Is Health IQ?

- How Does Health IQ Work?

- Health IQ Review: Where It Shines

- Health IQ Review: Where It Falls Short

- Examining Health IQ’s Term Life Insurance Product

- Other Health IQ Products

Health IQ Review: Quick Look

| Company Name | Health IQ |

|---|---|

| Company Type | Insurance comparison site or online broker |

| Key Features | Cheaper premiums for certain groups |

| Downsides | Long, convoluted application process |

| Best For | Healthy individuals |

What Is Health IQ?

Munjal Shah sold his first company to Google in 2010, reportedly for more than $100 million. Soon after, he ended up in the emergency room. He had chest pains while running a 10K race and thought he was having a heart attack.

The experience had a profound impact on Shah. He got serious about his health, losing 40 pounds. That led him to believe that individuals who work hard at diet and exercise should get rewarded with cheaper life insurance.

Shah founded Health IQ in 2013 based on that idea. The company raised money and rounded up data to make the case for lower rates based on certain qualifiers.

Health IQ works as an online insurance agent. It partners with more than two dozen insurance providers, secures rates and sends you offers to compare once you complete your application.

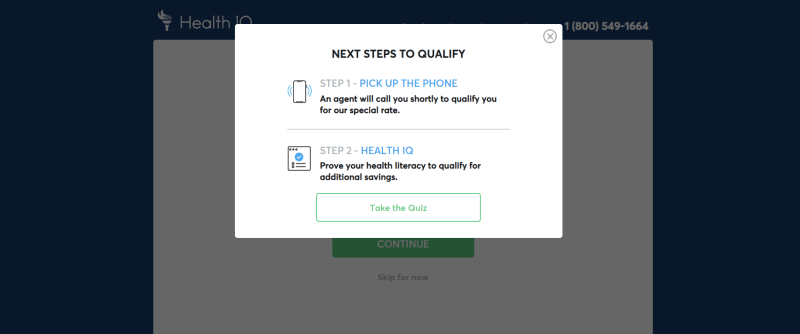

Individuals qualify for the lower insurance premiums that Health IQ secures based on the results of an in-home medical exam, their scores on health literacy quizzes and verification of their healthy lifestyles.

How Does Health IQ Work?

Health IQ makes it clear that it offers access to cheaper life insurance for the health-conscious.

It takes patience, persistence and lots of reading at healthiq.com to understand how the company achieves its discounted prices. To be fair, it’s too nuanced to explain quickly and easily. But how the company arrives at its rates may not be important to consumers as long as the prices are good.

Health IQ is a quote comparison site. It doesn’t underwrite its own insurance policies. Instead, when you finish your application, Health IQ sends your information to the insurance companies and then relays their offers to you.

Health IQ earns a commission if you purchase life insurance through its site.

How To Verify You’re Healthy Enough for Health IQ’s Special Rates

Health IQ says it has relationships with more than two dozen insurance companies. They offer customers special rates, provided you go through three verification methods designed to prove you’re in good health. You don’t have to nail all three prongs to get some kind of discount.

- Take a medical exam. Medical exams are a normal part of the life insurance buying process. The Health IQ version is tailored to athletes and active individuals. This is your opportunity to score the biggest savings on your premiums. Health IQ helps make sure that you don’t get penalized in the underwriting process (or that you even benefit) if you have a low resting heart rate as an endurance athlete, if you have a high BMI due to high muscle mass or if you have a certain waist-to-hip ratio (to name just a few test cases).

- Pass online health literacy quizzes. If you score well on Health IQ’s two online quizzes, the company says that proves you’re health-conscious. You can get an 8% discount on monthly premiums by “acing” the quizzes. I took and passed the first of those quizzes when going through the Health IQ application. It was a timed multiple-choice test about nutrition and exercise.

- Prove that you exercise. This is good for a 9% discount, according to Health IQ. There are several ways to tick this box, including running an eight-minute mile (or age-based equivalent), cycling 50+ miles per week, competing in a swim meet, deadlifting your body weight or holding a gym membership for at least one year. At the least, Health IQ’s verification process for this step seems scattered. You can provide this information to the company in several ways which include providing proof of gym membership, sharing exercise data from your fitness app or sharing athletic competition results.

Health IQ Review: Where It Shines

Here are some of Health IQ’s strong points:

- Significantly cheaper premiums for certain groups. If you’re measurably healthy, health-conscious and you have healthy habits, Health IQ may be able to get you much lower premiums. Term life insurance policies often cover 20+ years, so even small monthly savings can become significant.

- Wide range of carriers. The volume and prominence of Health IQ’s life insurance partners are similar to Policygenius, which is arguably the best-known insure-tech quote comparison site.

- Educational nutrition and exercise content. Vegetables are not traditionally a passion point for the average American. Health IQ didn’t invent this trick. But it takes subject matter that many people could find boring and gameifies it through a combination of quizzes, rewards, community and a leaderboard. Health IQ is an insurance company, not a health content site. But its My IQ hub offers a robust content library on nutrition and exercise.

- Likable theory. Health IQ is a for-profit business, but it’s easy to like its basic premise. If you work hard to exercise and eat healthily, you probably lower your risk of dying and should be rewarded with better insurance rates. Some specific use cases are comforting. For example, if your family has a negative health history but you have gone to great lengths to live a healthy lifestyle, Health IQ says it could likely still find a statistically-justified way to help you avoid full punishment from the risk-assessing algorithms.

Health IQ Review: Where It Falls Short

Here are some of Health IQ’s drawbacks:

- Long, complex application process. It takes considerable commitment and effort to get through the verification steps. That’s usually also true for the traditional life insurance buying process, which requires a medical exam. Some insure-tech companies are eliminating that step. But in addition to a medical exam, Health IQ also requires you to take quizzes, talk to a company representative and verify your lifestyle.

- Must provide personal information upfront. You can’t even begin the application process until you provide your home address, phone number, email address, and annual salary range.

- No price information on the site. There’s no way to get price quotes without going through the application process. Health IQ also seems to withhold some information on its site before you apply, such as how you verify your chosen fitness activity and the full list of insurance carriers with which it works.

Examining Health IQ’s Term Life Insurance Product

I tried going through the application process on Health IQ’s website.

First, it asks you for your name, age, gender, height, weight range, annual income range, phone number and email address. Then you have to talk to a Health IQ representative and take a multiple-choice quiz on health-related questions.

You can’t get a quote or move forward with the process unless you talk to a representative on the phone. And that’s easier said than done: Company representatives are only available during business hours (Pacific Time).

A Health IQ representative should be able to answer your questions, help you schedule your exam and give you instructions on how to verify your fitness activities.

The insurance companies that Health IQ works with include Prudential, Principal, Pacific Life, Ameritas, John Hancock, Lincoln Financial Group, Protective Life and SBLI. I was not able to find a full list of partners.

Health IQ facilitates term life insurance coverage of $100,000 to at least $10 million, a company representative said.

A Word of Caution on Health IQ’s Price Claims

Clark.com typically offers standard price quotes when reviewing any life insurance company. We always ask for quotes for 35- and 45-year-old females and males in excellent health from Florida. That way, when you read our site, you can compare apples to apples.

I was unable to get any quotes from Health IQ despite reaching out multiple times.

Therefore I can’t independently verify Health IQ’s claim that it can offer significantly lower monthly premiums to individuals in excellent health.

Other Health IQ Products

In addition to offering term life insurance, Health IQ offers:

- Guaranteed issue life insurance: This product doesn’t require a medical exam and offers up to $25,000 in coverage. Acceptance is guaranteed for people ages 50 to 85.

- Final expense insurance: Also called “funeral insurance,” this is a whole life insurance policy with a small death benefit. It’s easy to get approval, and it’s marketed as a way to pay for funeral and burial services.

- Auto insurance: Health IQ offers car insurance to drivers 65 and older. Customers must take Health IQ’s “SharpSenior” Quiz designed to measure reaction time, alertness and peripheral vision. Score well, and Health IQ says it can get you a discount from major car insurance carriers.

- Disability insurance: This type of insurance typically pays out if you miss work due to injury or illness. The Health IQ version requires the same application process that you’d go through to buy term life insurance. If you’re healthy, it’s possible that Health IQ can secure you a discounted rate.

- Medicare: Health IQ offers access to Medicare Advantage and Medicare supplement (Medigap) plans, which can cover some things that regular Medicare doesn’t. Health IQ says it can get special rates for the health-conscious.

Final Thoughts

If you consider yourself to be in great physical shape, Health IQ may be able to get you much cheaper premiums for your life insurance.

Health IQ’s application is long and involved. If that sounds onerous to you, you may be better off shopping with online insurance brokers or providers such as Policygenius, Haven Life or Fabric.

But if you meet all of Health IQ’s criteria and you want the cheapest possible rates for your term life insurance, wade through the application process. It’s could be worth doing if it helps you save significant money each month for 20+ years.

If you do buy a policy through Health IQ, remember that Clark recommends purchasing only from companies that have earned an A+ or A++ A.M. Best rating.